If you’re a company director and have ever dipped into company funds for a personal loan, you need to know about Section 455.

It’s a Corporation Tax charge that applies when director loans aren’t repaid on time – and it can be a costly surprise if you’re not prepared.

This blog explains what it is, how it works and how to stay on the right side of HMRC.

What is Section 455 tax?

Section 455 (or S455) is a Corporation Tax charge on loans from a ‘close’ company (which includes most small private limited companies controlled by five or fewer people) to a participator – usually a director, shareholder or someone connected to them.

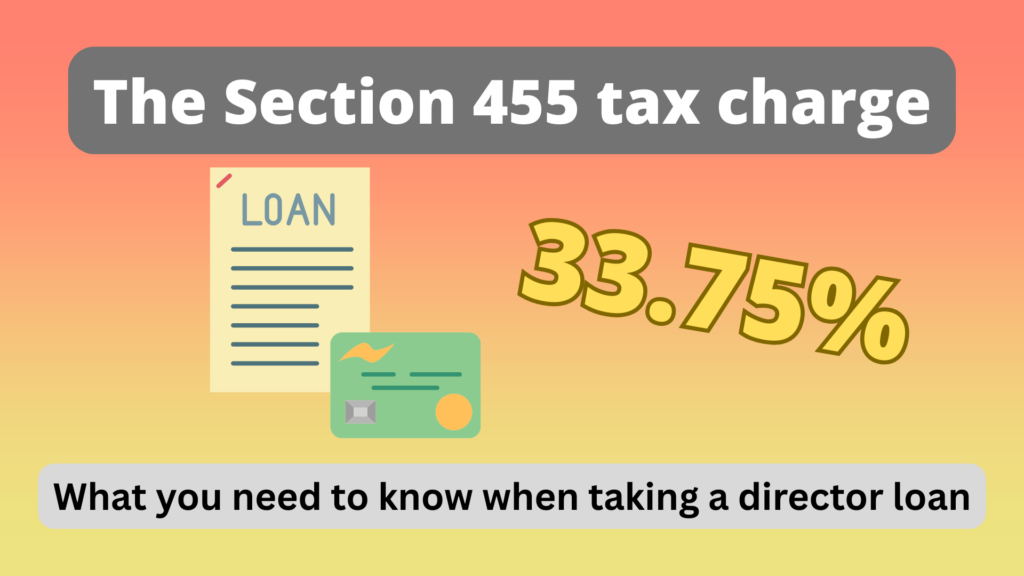

If you borrow money from the company and don’t repay it within nine months and one day after the company’s year-end, the business has to pay 33.75% of the outstanding amount to HMRC.

The charge isn’t permanent – once the loan is repaid, the company can reclaim the tax. But it still has to be paid upfront, which can put a strain on cash flow.

Here’s an example:

You borrow £10,000 from your company and miss the repayment deadline. Your business owes HMRC £3,375. If you repay the loan later, you’ll get that money back – but not quickly. HMRC refunds can take months.

Why does it exist?

Quite simply, HMRC doesn’t want directors taking money out of companies as ‘loans’ to avoid paying income tax or dividend tax. Aligning the S455 rate with dividend tax (33.75% in 2025) keeps things fair – and discourages directors from treating loans as a tax-free income stream.

When does S455 apply?

You’ll face an S455 charge if:

A director or shareholder borrows money from the company and that loan (or balance on a director’s loan account) isn’t repaid within nine months of year-end. The loan isn’t covered by an exemption.

S455 doesn’t just apply to money you take directly. Loans to family members, business partners or even through third parties can also be caught.

Are there any exemptions?

Yes. Not every loan triggers an S455 charge. Common exceptions include:

- Small staff loans: Where the loan is under £15,000 and made to a full-time employee who isn’t a shareholder.

- Trade credit: Normal business transactions, like unpaid supplier bills, as long as they’re settled within six months.

- Repayment on time: Clear the balance before the nine-month deadline, and there’s no charge at all.

But even if you avoid S455, large or interest-free loans over £10,000 may create a ‘benefit-in-kind’ for the director, which means extra personal tax and National Insurance for the company.

Common pitfalls

Directors often get caught out by:

- ‘Bed and breakfasting’: Repaying just before the deadline, then re-borrowing soon after. HMRC’s 30-day rule treats this as if the loan was never repaid.

- The £15,000 arrangements rule: Even outside the 30-day window, if there’s an agreement to borrow again, HMRC can still apply the tax.

- Multiple small loans: HMRC can combine them and treat them as one balance, so keeping good records is essential.

How to reclaim S455

Once a loan is repaid or cleared (for example, through a dividend), your company can apply for a refund. Claims are made either via the CT600 Corporation Tax return (if recent) or using form L2P for older loans.

The catch is that you’ll need to wait until nine months after the end of the accounting period in which the loan was repaid. In practice, this means the company may not see its money back for well over a year.

How to avoid S455 tax altogether

The best approach is prevention. Some smart steps include:

- Keeping your director’s loan account up to date with accurate bookkeeping.

- Declaring dividends properly (with board minutes and sufficient profits) rather than relying on informal withdrawals.

- Repaying loans in full and on time – and avoiding the temptation to reborrow straight away.

- Getting professional advice if you’re unsure, especially if loans are frequent or significant.

Summary

S455 tax isn’t the end of the world – but it can create an unnecessary cash-flow headache for businesses that don’t plan ahead. If you use director loans regularly, treat them with caution. Keep records, know your deadlines, and clear balances on time.

And if you’ve already paid S455 tax, remember it’s reclaimable – it just takes patience (and good paperwork). Make sure you understand how Section 455 works, as that can save your company money, hassle and prevent a few sleepless nights.

Understanding the rules around S455 tax can be complex, especially when director loans are used regularly as part of your company’s cash flow. At Wootton & Co, we help businesses avoid unexpected charges and keep tax bills under control. Get in touch today and let us help you.